Commercial auto insurance is one of the largest and most frustrating bills a small fleet owner pays. Premiums climb every year, claims swing renewal pricing in ways that feel disproportionate, and most fleet owners feel like passengers in the process rather than active participants. The good news, and the answer most readers come here looking for, is that yes, GPS tracking can lower what you pay for fleet insurance, but the size of the savings depends heavily on which carrier you use and how you use the data. Some carriers offer formal telematics discount programs and some do not. Even when your carrier does not have a program, behavior data gives you a credible negotiating tool at renewal that most small fleets never bring to the table. This article explains exactly how the savings work, what it takes to qualify, what to ask your broker, how to use telematics data as leverage with any insurer, and the realistic limits on how much you can expect to save.

How Insurers Price Commercial Fleet Coverage

Commercial auto pricing is, at heart, an exercise in estimating risk with limited information. An underwriter looking at a 10-truck plumbing fleet does not actually know how those trucks are driven. They cannot see actual speeds, late-night trips, hard acceleration patterns, or how often a driver slams on the brakes. So they fall back on proxies: the age and experience of the named drivers, the type and weight of the vehicles, the radius and territory the fleet operates in, the prior claims history of the business, and broad industry loss ratios. Each proxy is a coarse stand-in for the real underlying risk, and underwriters build a margin into the premium for the uncertainty those proxies leave on the table.

Telematics data shrinks that uncertainty. When an insurer can see, or at least see a credible report of, actual driver behavior, the risk picture sharpens. A fleet that looks average on paper but has clean speed, braking, and acceleration data is, in fact, lower risk than its profile suggests. Insurers that have a way to take that into account will reward the data, either through a formal usage-based discount or through more favorable underwriting decisions at renewal. That is the underlying reason GPS tracking can cut your premium: it replaces guesswork with evidence.

Three Ways GPS Tracking Lowers Your Bill

There are three distinct mechanisms at work, and they compound. The first is direct: a usage-based insurance (UBI) discount applied as a line item on your policy. The second is indirect but often larger over time: fewer at-fault accidents, which keeps your loss run clean and your renewal rates from climbing. The third applies specifically to comprehensive coverage: faster theft recovery and reduced loss exposure on stolen vehicles.

Usage-based insurance programs. A growing number of commercial carriers now offer formal UBI or telematics-based discount programs. Progressive Commercial, Nationwide, The Hartford, and Zurich all have versions of this for their commercial book of business. Discounts on these programs are typically in the 5 to 15 percent range, and in some cases up to 20 percent for fleets with strong data accumulated over a multi-year period. There is one important caveat: most formal UBI programs require the insurer's own device or an approved telematics partner, and they do not automatically accept a customer-submitted report from any GPS platform. That means you should not assume your telematics solution is plug-and-play with a specific insurer's UBI program. The right move is to ask your broker or commercial lines agent two questions: does my carrier have a telematics or usage-based discount program, and what device or partner do they require to qualify? Even when the answer is "you would need our device," the existence of these programs matters because it tells you what insurers in your market will pay for clean telematics data, which sets up the negotiating angle below.

Fewer accidents, cleaner loss runs. This mechanism gets discussed least and matters most over time. Multiple peer-reviewed studies and industry analyses have found that fleets using telematics-based driver coaching reduce collision frequency by 20 to 35 percent over the first year, with reductions of roughly 30 percent commonly reported once coaching is sustained over multiple quarters. Fewer at-fault claims means a cleaner three-year loss run, which is the single largest input into commercial auto pricing at renewal. A clean three-year loss run can save more on renewal pricing than any UBI discount, because it compounds: every year you avoid a major claim, your pricing baseline stays low. The Federal Motor Carrier Safety Administration's Large Truck and Bus Crash Facts reports hundreds of thousands of commercial vehicle crashes per year in the United States, with driver behavior factors (speeding, distraction, fatigue) consistently cited as leading contributors. Telematics directly addresses those leading causes, which is why the loss-run effect tends to be larger than the headline UBI discount over a three to five year horizon.

Theft recovery and lower comprehensive losses. Commercial vehicles are high-value theft targets. The FBI's Uniform Crime Reporting data has shown for years that work trucks and vans, often loaded with tools and equipment, are stolen at meaningful rates. Insurers price comprehensive coverage based partly on theft frequency and average loss severity. When a GPS tracker enables fast recovery, the loss severity drops sharply: the vehicle, and often the equipment inside it, comes back, and the claim is closed for a fraction of the replacement cost (or never filed at all). Carriers will sometimes price a fleet's comprehensive coverage more favorably when telematics is in use. More importantly, recoveries shift the ratio of claims paid to premiums collected, which is what carriers actually look at when deciding how to price you next year.

What Driver Behavior Data Insurers Actually Care About

Insurers do not just want raw GPS tracks. They want behavior signals that correlate with crash risk, and the same handful of metrics show up across every carrier's underwriting model and most of the academic literature.

Sudden braking. Frequent hard braking events correlate strongly with rear-end collisions and aggressive driving generally. Industry definitions tend to flag any deceleration above roughly 8 to 9 mph per second as a "harsh braking" event. A fleet with a low harsh-braking rate is, statistically, a lower rear-end-claim fleet, and that shows up directly in loss ratios.

Speeding. This is the headline metric for most insurers, both because it is easy to measure and because the data is unambiguous. Time and miles driven above the posted speed limit, especially sustained driving 5 to 10 mph over the limit, correlates with crash severity in addition to frequency. Even modest speeding meaningfully changes the cost of a claim when one happens.

Hard acceleration. Closely related to speeding and harsh braking, hard acceleration is treated as a marker for aggressive driving style overall. It is also a useful coaching signal because most drivers do not realize how often they do it until they see the data on a per-trip basis.

Late-night driving. Hours between roughly 10 PM and 5 AM have higher crash rates per mile driven, according to NHTSA research data. Some carriers' models weight late-night exposure heavily, especially for commercial vehicles where high after-hours mileage often signals either personal use of company vehicles or driver fatigue.

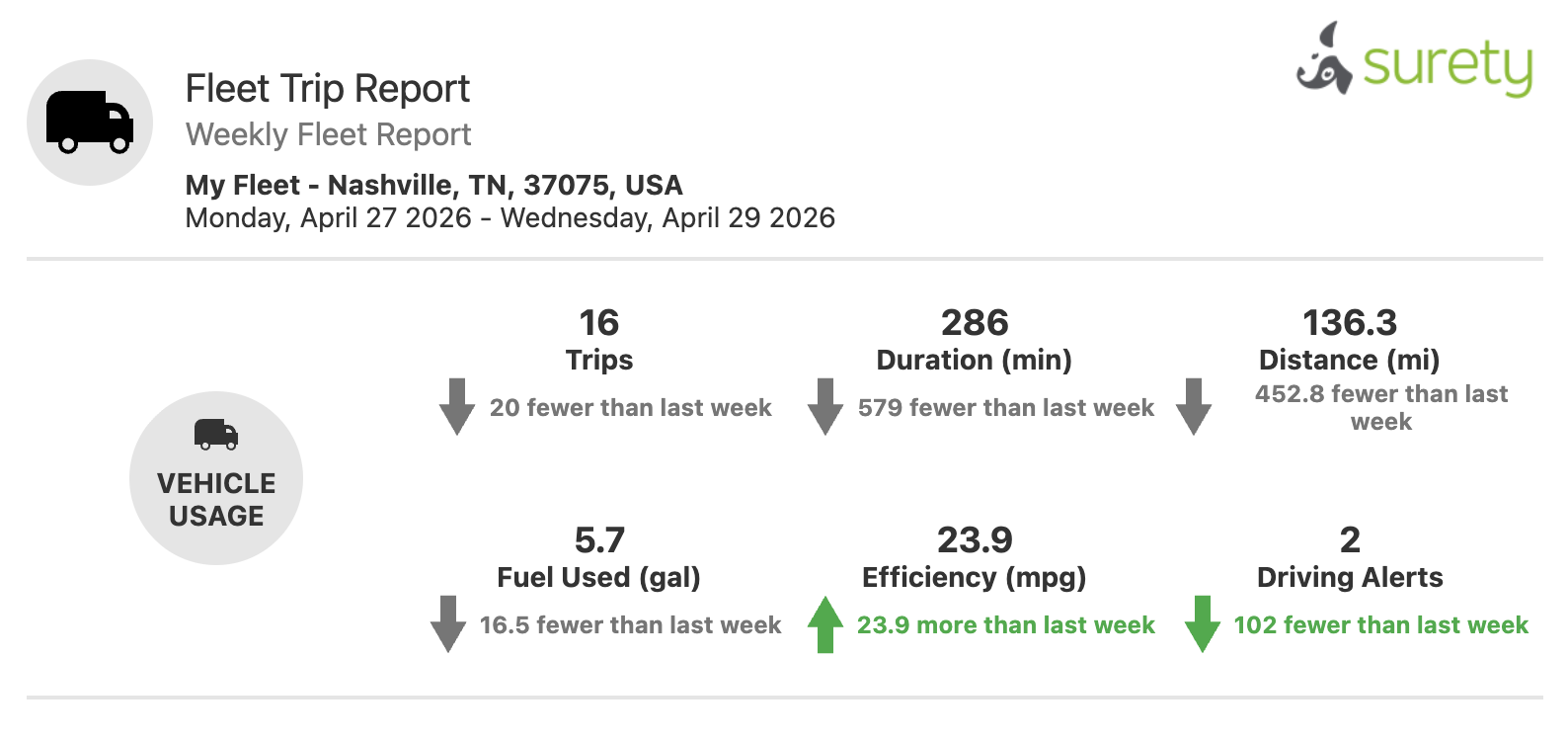

Alarm.com Connected Fleet captures all four of these. Speeding, hard acceleration, and sudden braking are tracked on every trip, alerted in real time when thresholds are crossed, and rolled up into Fleet Trip Reports that can be exported and emailed daily, weekly, or monthly. After-hours driving is covered separately, through Trip Started and Trip Ended Alerts that send notifications when a vehicle moves outside of business hours. Those alerts do not appear in the standard trip report, but the configured alert rules and the email history of received notifications are themselves documentation that you are actively monitoring for after-hours vehicle use, which is exactly what the underwriter wants to see. Together, this is the kind of evidence insurers respond to, and it is the same data a fleet manager uses internally to coach drivers.

The Underused Negotiating Tactic at Renewal

Most articles on this topic stop at usage-based insurance programs. Here is the part that gets less coverage and is more useful for small fleets: even insurers that do not have a formal telematics discount program will often improve renewal pricing if you can produce documentation of clean fleet behavior. Underwriters at every major commercial carrier are evaluated on loss ratio, and they have meaningful discretion at renewal. A 12-month report showing low harsh-braking rates, minimal speeding, and consistent on-route driving gives the underwriter a concrete reason to keep your pricing flat or reduce it, even without a formal program to plug into.

Most small fleet owners never use this tactic, because they do not have the data to bring to the meeting. Walking into a renewal with a printed Fleet Trip Report changes the conversation. Even in the worst case, where the carrier will not budge, that same data lets you shop the account to a competing carrier that does have a UBI program, and the competing quote will be priced more favorably than it would have been without the supporting evidence. Either way, you are using the data as leverage instead of leaving it sitting in a dashboard nobody outside the business ever sees.

How to Actually Get the Discount

The path from "we have GPS tracking" to "we are paying less for insurance" is not always automatic. Here is the practical sequence that works for most small fleets.

-

Install GPS tracking on the majority of fleet vehicles. Some carriers will only credit a telematics program if the fleet is at least 80 percent covered. With Alarm.com Connected Fleet, installation is a five-minute plug into the OBD-II port on each vehicle, so this step is almost always feasible across the entire fleet rather than just a sample.

-

Run the system for 60 to 90 days before approaching your insurer. You want a meaningful baseline of behavior data, and you want time to address any obvious problems (a single driver with chronic harsh braking, a route that produces unnecessary speeding) internally first. Three months is enough to show a representative pattern and to let initial coaching take effect.

-

Pull a fleet behavior report from the dashboard. Connected Fleet generates daily, weekly, and monthly Fleet Trip Reports that include the metrics insurers care about: speeding, hard acceleration, sudden braking, and trip-level route and timing history. Export the most recent 60 to 90 days as a PDF or spreadsheet.

-

Call your commercial insurance broker or your carrier's commercial lines department. Ask the specific question: "Do you offer a telematics or usage-based discount for commercial fleets, and if so, what device or partner do you require?" Brokers do not always volunteer this information, so asking by name forces a clear answer.

-

Submit the telematics report as supporting documentation at your next renewal. Even when there is no formal program, attach the report to your renewal application. It signals to the underwriter that you are an actively managed fleet, which is itself a risk indicator.

-

If your current insurer has nothing to offer, use the data as leverage with competing carriers. Brokers can shop the account to multiple markets. Carriers with formal UBI programs will price you more favorably when they can see clean behavior data going into the quote, even if the program ultimately requires switching to their device after binding.

A Worked Example: ROI on a 10-Vehicle Fleet

Numbers help. Consider a 10-vehicle plumbing company. Industry estimates put commercial auto premiums for small business vehicles in the $1,200 to $2,400 per vehicle per year range, depending on vehicle type, driver history, and coverage level. Assume the middle of that range at $1,800 per vehicle, so the fleet is paying $18,000 a year in commercial auto premium.

Alarm.com Connected Fleet through Surety Business runs roughly $12 per vehicle per month, or about $144 per vehicle per year, with a one-time $99 hardware cost per vehicle that works out to about $200 per vehicle per year all-in over the first three years. That puts the system cost for the 10-vehicle fleet at approximately $2,000 per year. If the fleet earns a 10 percent telematics discount on its commercial auto premium, the insurance saving is $1,800 per year. The math, simplified:

Net annual benefit = Insurance savings − GPS tracking cost = $1,800 − $2,000 ≈ break even

On insurance savings alone, the system pays for itself, give or take a few hundred dollars in either direction depending on your specific premium, your specific discount, and your fleet size. That is already a defensible spend. The actual ROI case is much stronger once the other categories that GPS tracking improves are layered in: fuel savings, dispatch productivity, lower maintenance through OBD-II diagnostic alerts, theft prevention, and the compounding effect of a cleaner loss run year after year. Insurance is one of five buckets where this system pays back, not the only one. For a full breakdown of the other categories, see How to Calculate the ROI of Fleet Tracking for a Small Business.

Caveats: Where This Gets Complicated

A few honest notes are worth making here, because the savings story has real limits.

Not every carrier has a program. Telematics discounts are not standard across the commercial auto market. Coverage and discount availability vary by state, by carrier, and by line of business. If your current carrier offers nothing, the direct UBI line in the math above drops to zero until you switch carriers or until your carrier rolls out a program.

Discounts apply at renewal, not mid-term. Even when a discount is available, it shows up at your next policy renewal, not the day you install the trackers. Plan for a 6 to 12 month lag between starting the program and seeing the savings on your bill.

The data can theoretically work against you. If your fleet's first 60 days of behavior data shows persistent speeding, harsh braking, and after-hours misuse, sharing that report with an insurer too early could result in worse pricing rather than better. The right sequence is: install the system, use the data internally first to coach drivers and clean up the worst patterns, and only share the report with insurers after behavior has improved. This is one reason the 60 to 90 day waiting period in the step-by-step section matters.

Subscription cost is a real line item. Whatever discount you negotiate has to clear the cost of the system. At Alarm.com Connected Fleet's pricing through Surety Business (typically $12 per vehicle per month for fleets of 2 to 20 vehicles), many small fleets find that the insurance savings alone roughly offset the system cost, and the rest of the ROI comes from fuel, productivity, and theft prevention. If your fleet is unusually small or your insurance premium is unusually low, the insurance line by itself may not justify the spend, and you should evaluate the full ROI picture instead of relying on insurance savings alone.

Frequently Asked Questions

- Does GPS tracking automatically lower my fleet insurance?

No. Installing tracking by itself does not change your premium. The savings come from one of three pathways: a formal usage-based insurance program where the carrier credits a discount in exchange for behavior data, a cleaner multi-year loss run that improves your renewal pricing, or using the data as leverage to negotiate at renewal or with competing carriers. All three require you (or your broker) to take action.

- Which insurance companies offer telematics discounts for small fleets?

Programs are available from Progressive Commercial, Nationwide, The Hartford, and Zurich, among others. Availability varies by state and by the size and class of the fleet. Ask your commercial insurance broker which carriers in your state have a current program for fleets your size, and what device or partner they require to qualify.

- How much can GPS tracking reduce my commercial auto insurance?

Formal UBI program discounts typically run 5 to 15 percent, occasionally up to 20 percent for fleets with strong multi-year data. The larger long-term saving usually comes indirectly, through fewer at-fault claims and a cleaner loss run, which compounds at every renewal.

- How long does it take to see insurance savings after installing GPS tracking?

Plan on 6 to 12 months. Discounts apply at renewal rather than mid-term, and most carriers want at least 60 to 90 days of behavior data before crediting a telematics-based discount. The compounding benefit of fewer claims plays out over multiple renewal cycles.

- Can telematics data be used against me by my insurer?

In a formal UBI program, only the data the program is designed to use is shared, and that data is structured to lower your rate (programs are designed as discount mechanisms, not surcharge mechanisms). Outside of formal programs, you control what you share. If your fleet's behavior baseline is poor, do not share the report with insurers until you have coached drivers and cleaned up the data internally. Telematics works best when you use it to fix problems first and document improvement second.

- Do all vehicles in my fleet need GPS tracking to qualify for a discount?

For most formal UBI programs, yes, or at least a high majority (commonly 80 percent or more of the fleet). Carriers do not want to credit a fleet-wide discount based on a few sampled vehicles. With Alarm.com Connected Fleet's $12 per vehicle per month pricing and five-minute plug-in installation, equipping the entire fleet is usually straightforward.

The Bottom Line

Fleet insurance is one of the few major operating costs where most small fleet owners assume they have no leverage. Telematics changes that. Whether through a formal usage-based program, a cleaner loss run, faster theft recovery, or simply a credible report you bring to your renewal meeting, GPS tracking gives the underwriter something specific to price against, and it gives you a tool for negotiation that most small fleet owners never use. The carriers that have a program will reward the data directly. The carriers that do not will still respond to evidence at renewal. Either way, fleet owners who are not using their telematics data as a negotiating tool at renewal are leaving money on the table that more disciplined competitors are starting to collect.